Navigating Non-Performing Assets: Strategies for Effective Management

Introduction:

Non-Performing Assets (NPAs) are a common concern in the financial world, affecting both lenders and borrowers. They represent loans that have stopped generating income for the lender, usually due to the borrower’s failure to make timely repayments. NPAs can pose significant challenges to financial institutions, impacting their profitability and stability. However, with proper management strategies, the adverse effects of NPAs can be mitigated.

Navigating Mutual Funds: A Comparative Analysis of Public and Private Options secret 2024

Understanding Non-Performing Assets:

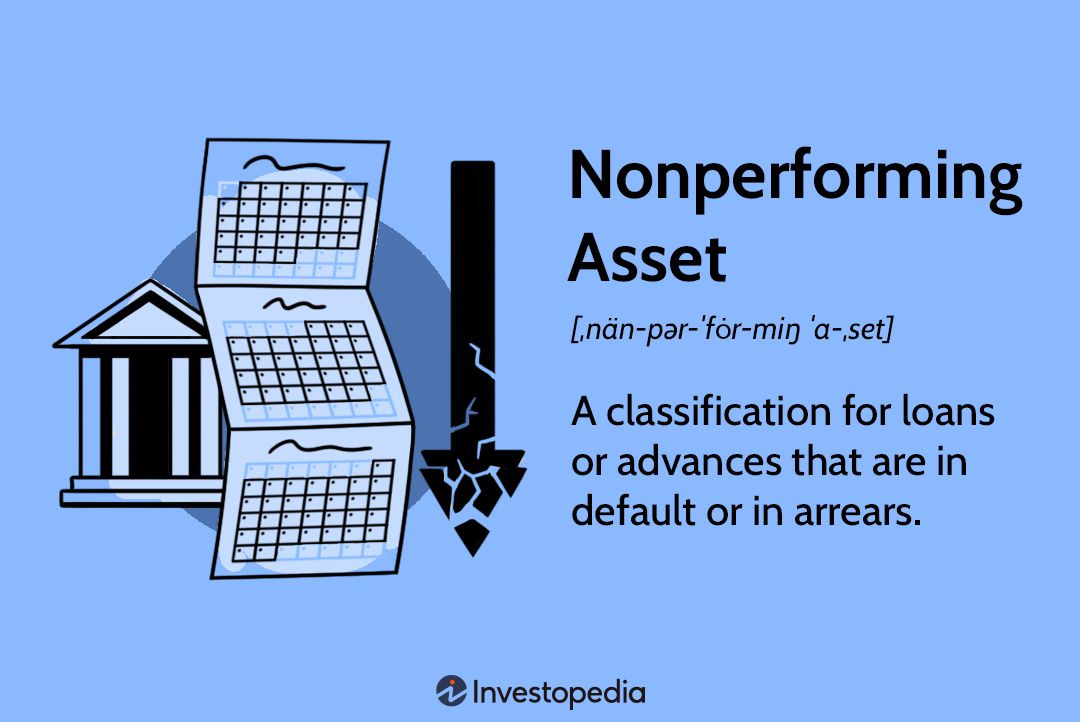

NPAs typically include loans, advances, or credit facilities where the interest or principal remains unpaid for a specified period, usually 90 days or more. These assets signal potential risks to the financial health of banks and other lending institutions. They arise from various factors, including economic downturns, borrower insolvency, or poor credit assessment processes.

Challenges Associated with NPAs:

The presence of NPAs presents several challenges for financial institutions:

- Reduced Profitability: NPAs lead to a decrease in interest income, affecting the overall profitability of the lender.

- Capital Adequacy Concerns: Regulatory authorities require banks to maintain a certain level of capital adequacy to absorb potential losses. High levels of NPAs can strain a bank’s capital reserves, jeopardizing its ability to meet regulatory requirements.

- Reputational Risk: A high NPA ratio can erode investor confidence and tarnish the reputation of the lending institution.

- Liquidity Issues: NPAs tie up funds that could otherwise be deployed for productive lending activities, limiting liquidity and hindering growth opportunities.

Effective Management Strategies

To address NPAs proactively, financial institutions employ various management strategies:

- Early Detection and Risk Assessment: Timely identification of potential NPAs is crucial. Banks use advanced analytics and risk assessment models to identify borrowers at risk of default and take preventive measures.

- Restructuring and Resolution: Banks may opt for loan restructuring or renegotiation of terms to help distressed borrowers repay their debts. Restructuring involves modifying the loan terms, such as extending the repayment period or reducing interest rates, to make it more manageable for the borrower.

- Asset Quality Review: Conducting periodic asset quality reviews enables banks to assess the health of their loan portfolios and identify NPAs early on. This process involves classifying assets based on their credit quality and assessing the adequacy of provisions.

- Recovery and Rehabilitation: Financial institutions pursue recovery and rehabilitation measures to recover dues from defaulting borrowers. This may involve legal recourse, asset seizure, or engaging with debt recovery agencies to recover outstanding amounts.

- Prudent Lending Practices: Adopting sound lending practices and conducting comprehensive credit assessments can help mitigate the risk of NPAs. Banks should evaluate the creditworthiness of borrowers and establish robust risk management frameworks to minimize NPA-related risks.

Conclusion:

https://ahrefs.com/

Non-Performing Assets pose significant challenges to the financial stability and profitability of lending institutions. However, with effective management strategies, including early detection, restructuring, and prudent lending practices, banks can mitigate the impact of NPAs and safeguard their financial health. By adopting proactive measures and embracing technological innovations, financial institutions can navigate the complexities of NPAs and foster a healthier lending ecosystem.

[…] Navigating Non-Performing Assets: Strategies for Effective Management secret human 2024 […]